With a combined population of approximately 140 million (over 40% of the U.S. total), Gen Z (born 1997–2012) and Millennials (born 1981–1996) are increasingly favoring rental housing over homeownership. This shift is driven by a confluence of economic, social, and lifestyle factors. Recent reports indicate that existing home sales in 2024 have fallen to their lowest point since 1995, further underscoring this trend and reshaping the U.S. housing market, creating significant opportunities for the multifamily rental sector.

A 2022 Apartment List survey revealed that nearly 25% of millennial renters plan to rent indefinitely, almost double the 13% who expressed this intention in 2010. Nearly 75% of these renters cited affordability as the primary barrier to homeownership. ELIM anticipates these trends will persist, as homeownership remains out of reach for many Americans, fueling demand for both traditional multifamily and built-for-rent communities.

The rising costs of homeownership, including maintenance, insurance, and property taxes, coupled with 30-year fixed mortgage rates forecast to remain around 6-7% in 2024 and 2025, are expected to perpetuate the housing affordability challenge. As homeownership becomes more expensive, the renter population grows. The rentership rate compared to the homeownership rate in the 75 largest U.S. metropolitan areas has increased significantly in the past four to five years, coinciding with a median home price increase exceeding 70% since 2018.

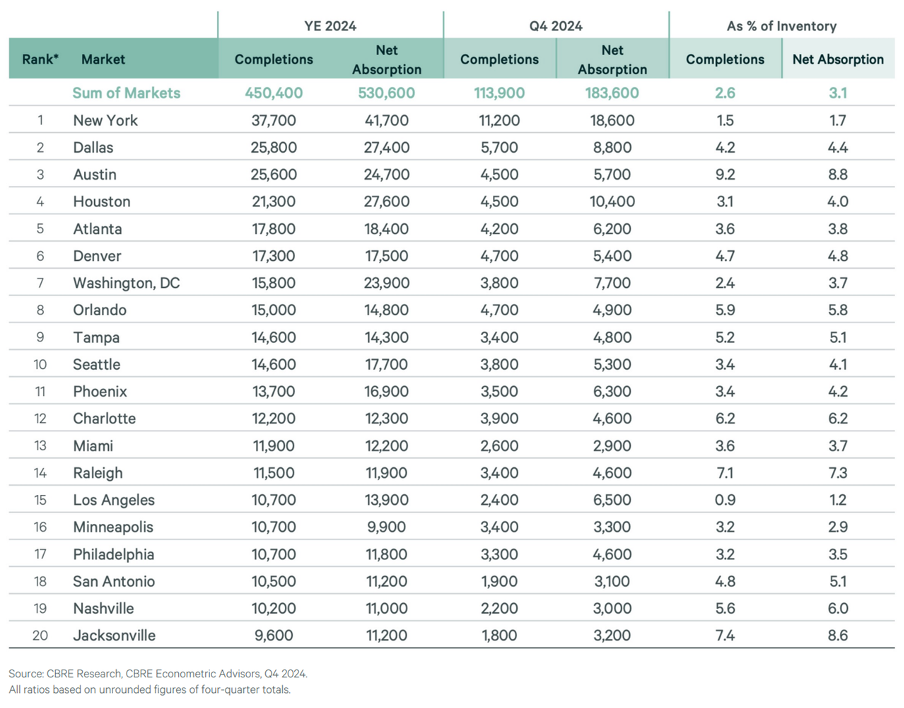

Newly released 2024 multifamily data shows annual net absorption reaching 530,600 units, more than double the 248,800 units absorbed in 2023. Annual net absorption exceeds completions in most markets, primarily driven by positive job growth and net migration.

Gen Z and Millennials: A Continued Shift Toward Rentals

A recent study by the National Association of Realtors indicates that the median age of first-time homebuyers has risen to 38 in 2024 and is expected to remain elevated in 2025. In 2025, the oldest members of Gen Z will be 28, entering their prime renting years. With approximately 68 million Gen Z members, a new wave of renters is expected to enter the market in the next three to five years, significantly increasing demand for multifamily housing. Of the approximately 72 million Millennials, an estimated 40-45% will remain renters due to affordability challenges and lifestyle preferences.

Younger generations continue to gravitate toward cities and suburbs with strong job markets, where renting is often more practical than buying. They value flexibility and mobility, often prioritizing career opportunities and urban living over long-term homeownership. Renting facilitates easier relocation. Furthermore, Millennials and Gen Z are delaying marriage and having children compared to previous generations, lessening the urgency to buy a home. Urban living is also more appealing, as many younger renters prefer proximity to work, entertainment, and social activities, where renting is often more feasible.

A Generational Shift Toward Renting

Gen Z and Millennials are increasingly choosing rental housing due to affordability issues, lifestyle choices, and economic uncertainty. Driven by strong rental demand, the U.S. will need 4.3 million new apartments by 2035 to meet demand, according to the National Multifamily Housing Council (NMHC). Rent growth is expected to stabilize at 2-4% annually in some markets as completions decrease from 2025 onward due to high development costs and interest rates in 2023/2024. A significant portion of this multifamily demand will originate from Gen Z and Millennials. This trend is reshaping the multifamily market, creating opportunities for investors and developers to cater to the needs of younger renters.

Investing in multifamily assets is a long-term strategy. The ELIM Investment Team is carefully selecting prime investments in today’s challenging market, navigating interest rates, inflation, and economic shifts with data-driven decision-making. Within our builder network, we are constantly evaluating opportunities in both overbuilt and supply-constrained markets for development and acquisition, as well as exploring value-add recapitalization projects for investment in 2025.